Celebrating as a family member graduates high school and attends college is a joyous event and the culmination of years of hard work. However, paying for college remains a significant source of stress for many households. It's no secret that the cost of college has risen much faster than inflation over the past 40 years, increasing the financial burden on families as they set money aside and on graduates once they enter the workforce. And yet, there are numerous professional and personal benefits to pursuing higher education for those who wish to do so. Weighing the costs against the benefits, while considering personal priorities and the broader economic picture, makes college planning a complex topic.

THERE ARE MANY ECONOMIC BENEFITS TO ATTAINING HIGHER LEVELS OF EDUCATION

This is why saving for college is a core component of any financial plan alongside other major goals such as retirement or buying a home. With all of the market and economic uncertainty of the past decade, customizing a financial plan to each individual or household's needs, ideally with the guidance of a trusted advisor, has never been more important. What should those planning for college consider today?

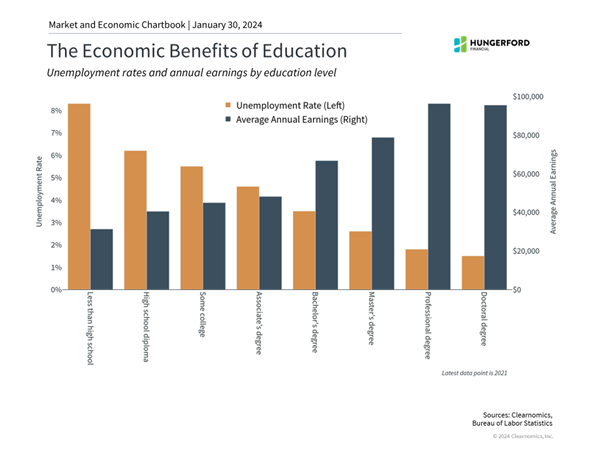

The rapid increase in the cost of education has led many to question whether college is still worth the investment. An important reason tuitions have risen so rapidly is that the economic benefits of college and advanced degrees have grown even faster. According to the Bureau of Labor Statistics, job prospects improve as educational attainment increases. For example, the accompanying chart shows that unemployment rates were 6.2% for high school graduates but only 3.5% for those with 4-year bachelor's degrees. Similarly, the median annual earnings of those with high school diplomas was $40,450 compared to $66,700 for college graduates. Not surprisingly, these patterns continue for advanced degrees as well.

Of course, these statistics are averages that don't consider individual circumstances or differences within each education level. Pursuing college and advanced degrees may not be for everyone, and there are many personal factors that must be considered. For instance, today's very low unemployment rates may make the opportunity costs of attending a 4-year college less attractive to some, including those who attend trade schools or benefit from on-the-job training. In contrast, poor economic periods such as during the global financial crisis may make the benefits of college more pronounced.

Additionally, these particular statistics don't consider the choice of college major or type of employment. It's clear that those studying highly employable subjects, such those related to engineering and financial services, will likely have greater job prospects. Regardless, the broad data make it clear that there are many economic benefits to higher education.

THE COST OF A COLLEGE EDUCATION HAS RISEN MUCH FASTER THAN INFLATION

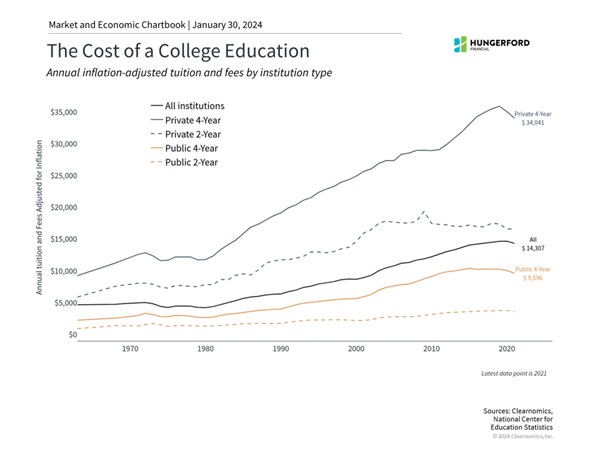

As a client, it's important to be aware of the significant increase in the cost of a college education over the past four decades. The sticker price of college has surged by a staggering 800%, even after adjusting for inflation. Private 4-year colleges have witnessed a 176% real, inflation-adjusted cost increase, and public universities have experienced a 252% rise. Even 2-year degrees have risen above inflation in most years. This concerning trend has created financial challenges for those seeking higher education, and it's crucial to address this issue.

Given the disproportionate growth in education costs compared to wage increases, financial planning for college is of utmost importance. To cope with these costs, individuals and families need to start saving early, save more, leverage investment returns, and consider borrowing. Investment vehicles like 529 plans come with tax benefits and are designed to encourage early savings to take advantage of compound interest over time. Recent data by Sallie Mae reveals that families typically fund 43% of college costs through parents' income and savings, 11% through the student's contributions, 29% through scholarships, grants, and help from relatives, and 18% through borrowing. Therefore, the decision on how to finance college necessitates a thorough understanding of your unique circumstances.

Considering the long-term implications, early planning for your child's college education is wise, as it allows you to harness the power of compound interest. It's also prudent to begin exploring college options early and comparing costs to make well-informed decisions that can lead to a better financial outcome. The rising cost of education is a reality, but with thoughtful financial planning and an understanding of the available options, you can navigate this challenge and make college more affordable and accessible for your family.

STUDENT LOANS ARE A MAJOR BURDEN ON CONSUMERS

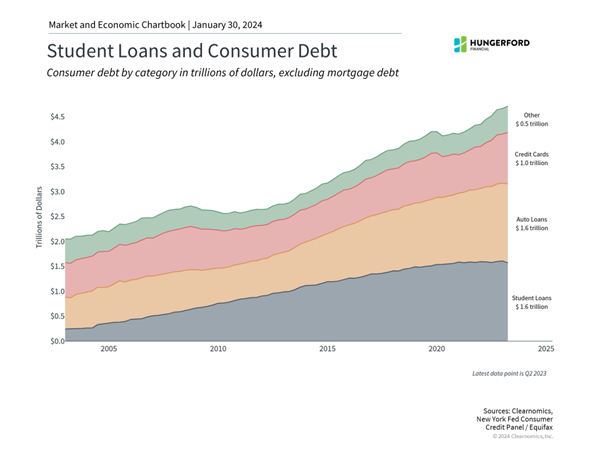

Unfortunately, borrowing for college often results in high levels of student loan debt upon graduation. At the individual level, this is a burden on graduates that must be factored into every financial and career decision. In the worst case, it may mean that graduates are unable to take as many risks or pursue their true passions if it means they are unable to generate the steady income needed to repay their loans.

At the aggregate level across the economy, student loans have ballooned over the past 20 years to $1.6 trillion, outpacing other non-mortgage consumer debt. This has led to macroeconomic concerns with some comparing the size of student loan debt to the subprime crisis prior to 2008. While it's difficult to say exactly how this will impact the economy, there are important differences to subprime loans such as grace periods, forbearance, parent cosigners, and more. Still, it's possible that high levels of student debt could act as a drag on the economy due to its influence on career decisions, reduced consumer spending, and more.

Of course, the student debt crisis has become a key political issue. The current administration recently sought to cancel up to $20,000 in federal student loans for qualified borrowers. However, the Supreme Court has ruled that this is an overstep of the executive branch and invalidated the action. Politics aside, this has resulted in uncertainty for those with student loan bills coming due.

The bottom line? Higher education continues to be extremely valuable from a financial and economic perspective. Deciding how to pay for college is an important component of any financial plan. Saving early, making appropriate investments, and using attractive vehicles, can help to increase the odds of financial success. If you have a current high schooler and are interested in starting the process of reviewing colleges and what the cost will look like please be sure to reach out to us.

This content is developed from sources believed to be providing accurate information. It is meant for educational purposes only and should not be considered specific advice. Always consult with a financial professional regarding your personal situation before making any financial decisions.